Use our mortgage deed to give a lender security interest in real property the borrower is financing.

Updated August 9, 2024

Written by Sara Hostelley | Reviewed by Susan Chai, Esq.

A mortgage deed or mortgage agreement is a written document officially recognizing a legally binding relationship between a borrower and lender. When a borrower takes out a loan to purchase a real estate property, they agree to pay the lender back for the loan through this document.

Under its terms, the borrower maintains real estate property ownership, so they can use it as they see fit. During the repayment period, the lender, usually a bank or financial institution, maintains an interest in the real estate property.

This security interest, called a mortgage, allows the lender to recover the property if the borrower fails to pay. If the borrower fails to adhere to the mortgage agreement terms, the lender can take possession of the property through foreclosure. They can also pursue reasonable attorney’s fees incurred.

You can use a mortgage deed if you loan money to another person and want to keep a security interest in the property until they pay back their debt. Alternatively, you can initiate a mortgage deed if you want to borrow money and offer the property you’re purchasing as a security to the lender that you’ll meet your repayment obligations.

Some specific use cases for this document include:

A simple mortgage contract generally includes the following elements:

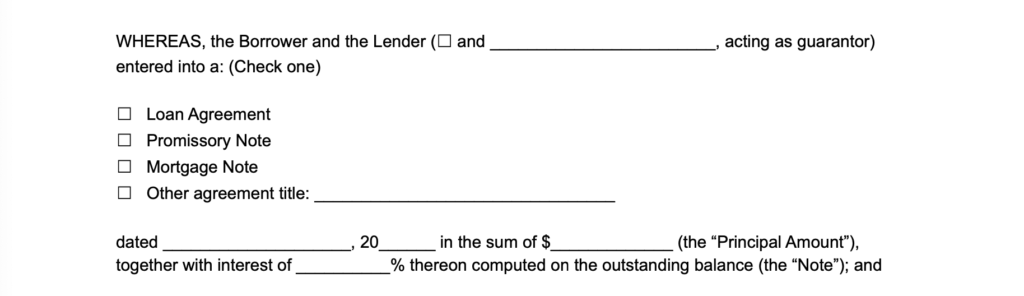

A mortgage deed should clearly state the amount of money borrowed (the principal amount), the interest rate charged, and the principal (the interest amount) agreed upon in the loan agreement or promissory note.

A mortgage deed involves several steps to create a concise and legally binding relationship between a borrower and a lender. It begins with a loan agreement that the borrower (the mortgagor) and the lender (the mortgagee) enter into. Within this agreement, they outline the loan’s terms and conditions.

Once they settle on these details, they begin writing the deed. Within this deed, they highlight the borrower’s agreement to give the lender a lien on the property. This document also covers details like the property description and unique mortgage covenants.

From there, the following steps occur:

A mortgage deed and a deed of trust create a lien on a property to secure loan repayment. Some states allow one or the other, while others permit both. Explore their key differences below:

Here’s a list of states that allow mortgage deeds and deeds of trust:

| State | Mortgage Deeds Permitted? | Deeds of Trust Permitted? |

|---|---|---|

| Alabama | Yes | Yes |

| Alaska | No | Yes |

| Arizona | Yes | Yes |

| Arkansas | Yes | Yes |

| California | No | Yes |

| Colorado | No | Yes |

| Connecticut | Yes | No |

| Delaware | Yes | No |

| District of Columbia | No | Yes |

| Florida | Yes | No |

| Georgia | No | Yes |

| Hawaii | No | Yes |

| Idaho | No | Yes |

| Illinois | Yes | Yes |

| Indiana | Yes | No |

| Iowa | Yes | Yes |

| Kansas | Yes | No |

| Kentucky | Yes | Yes |

| Louisiana | Yes | No |

| Maine | No | Yes |

| Maryland | Yes | Yes |

| Massachusetts | No | Yes |

| Michigan | Yes | Yes |

| Minnesota | No | Yes |

| Mississippi | No | Yes |

| Missouri | No | Yes |

| Montana | Yes | Yes |

| Nebraska | No | Yes |

| Nevada | No | Yes |

| New Hampshire | No | Yes |

| New Jersey | Yes | No |

| New Mexico | Yes | Yes |

| New York | Yes | No |

| North Carolina | No | Yes |

| North Dakota | Yes | No |

| Ohio | Yes | No |

| Oklahoma | Yes | No |

| Oregon | No | Yes |

| Pennsylvania | Yes | No |

| Rhode Island | No | Yes |

| South Carolina | Yes | Yes |

| South Dakota | Yes | Yes |

| Tennessee | No | Yes |

| Texas | No | Yes |

| Utah | No | Yes |

| Vermont | Yes | No |

| Virginia | No | Yes |

| Washington | No | Yes |

| West Virginia | No | Yes |

| Wisconsin | Yes | No |

| Wyoming | No | Yes |

| Show More Show Less | ||

Within a mortgage deed, the lender must ensure the borrower meets their payment obligations.

Within a deed of trust, a trustee holds the borrower’s title in escrow until they meet all their payment obligations. The trustee can initiate foreclosure on the lender’s behalf if the borrower doesn’t make their payments.

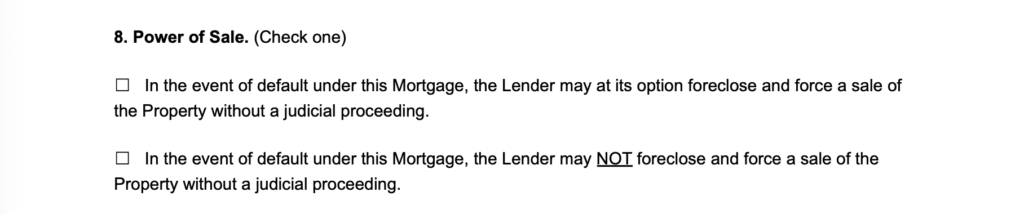

One of the significant differences between this agreement and a deed of trust is the lender’s remedy if the borrower defaults.

The lender must obtain a court order through the judicial process to take control of the property in foreclosure. Depending on the court’s calendar, the strength of the borrower’s defenses, and other procedural requirements, the foreclosure process could take several months to a few years.

If a deed of trust has a “power of sale” clause (and most do), the trustee can foreclose on the property without a court order.

The non-judicial foreclosure process can be completed within two to three months.

However, each state has its rules, notice periods, and judicial and non-judicial foreclosure procedures so timelines may vary. Lenders must strictly follow these rules to avoid any challenges to the foreclosure sale.

Certain states also have a redemption period, giving the borrower a certain amount of time to buy back the property.

Here’s a summary of the differences between the two documents:

| Mortgage Agreement | Deed of Trust |

|---|---|

| Who are the parties: | Borrower |

In addition to a mortgage deed and a deed of trust, there are other common types of deeds. Each one offers a different degree of protection during a real estate transaction. Make sure you select the correct type of deed for the sale or transfer of your property or piece of land.

Before you fill out your mortgage deed form, write your state at the top.

1. Date of Deed. Provide the effective date of the mortgage agreement.

2. Borrower. Write the full name of the borrower, the party receiving the loan and pledging the property. If there is more than one borrower, provide all borrowers’ names. Write the borrower’s street address.

3. Lender. Write the lender’s full name, the party granting the loan and receiving a lien on the property. Provide the lender’s street address.

4. Guarantor. State any guarantor on the loan agreement or note. If there is a guarantor, provide the person’s full name.

5. Name of Agreement or Note. Provide the full name or title of the agreement or promissory note that details the loan between the borrower and lender. You may need an affidavit of title to show proof of title. Also, provide the date of the loan agreement or note.

6. Principal Amount. Specify the total principal amount of the loan and the interest rate.

7. Property Address. Enter the street (physical) address of the mortgaged property pledged as security for the mortgage loan. Include any unit or apartment number, if applicable.

8. Legal Description. Write the legal description of the property. A legal description is a geographical description of the property, commonly identified by a government survey, metes and bounds, or lot and block. You can find the legal description on the property’s deed or tax assessment or through the county registrar or assessor.

9. Assigned Rents. State whether the borrower will collect rent on the property.

10. Acceleration. Specify the days the borrower can default before the lender can accelerate the loan.

11. Power of Sale. State whether the lender can foreclose and sell the property without going through the judicial property in case of a default.

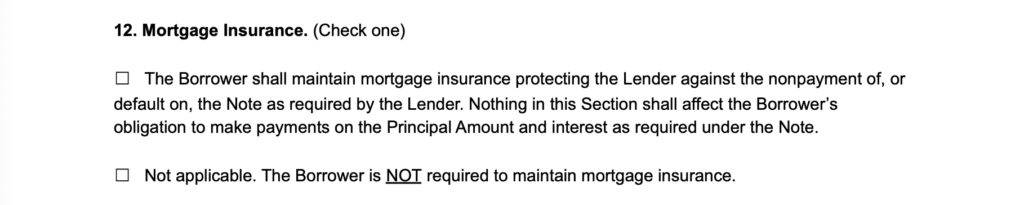

12. Mortgage Insurance. Specify whether the borrower must carry mortgage insurance that protects the lender if the borrower defaults on payments.

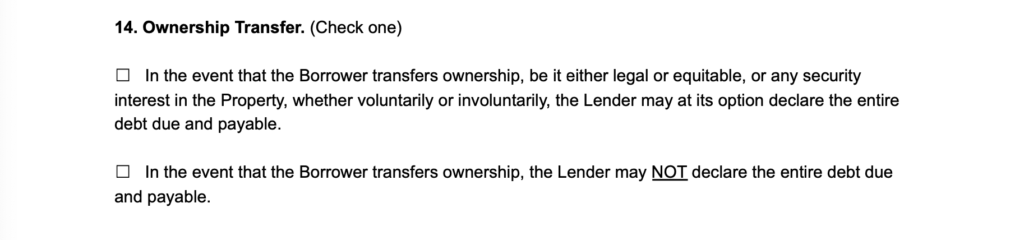

13. Ownership Transfer. State whether the lender can make the entire loan balance due and payable immediately if the borrower transfers ownership of the property.

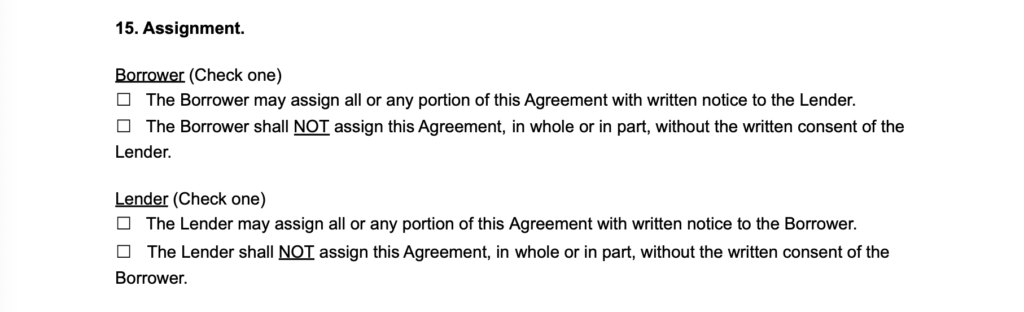

14. Borrower. Specify whether the borrower can assign an interest in the agreement without the lender’s permission.

15. Lender. State whether the lender can assign an interest in the agreement without the borrower’s permission.

mortgage deed assignment" width="1024" height="312" />

mortgage deed assignment" width="1024" height="312" />

16. State Law. Choose the state’s laws that will govern the deed.

17. Additional Details. You can include other provisions in our mortgage deed template.

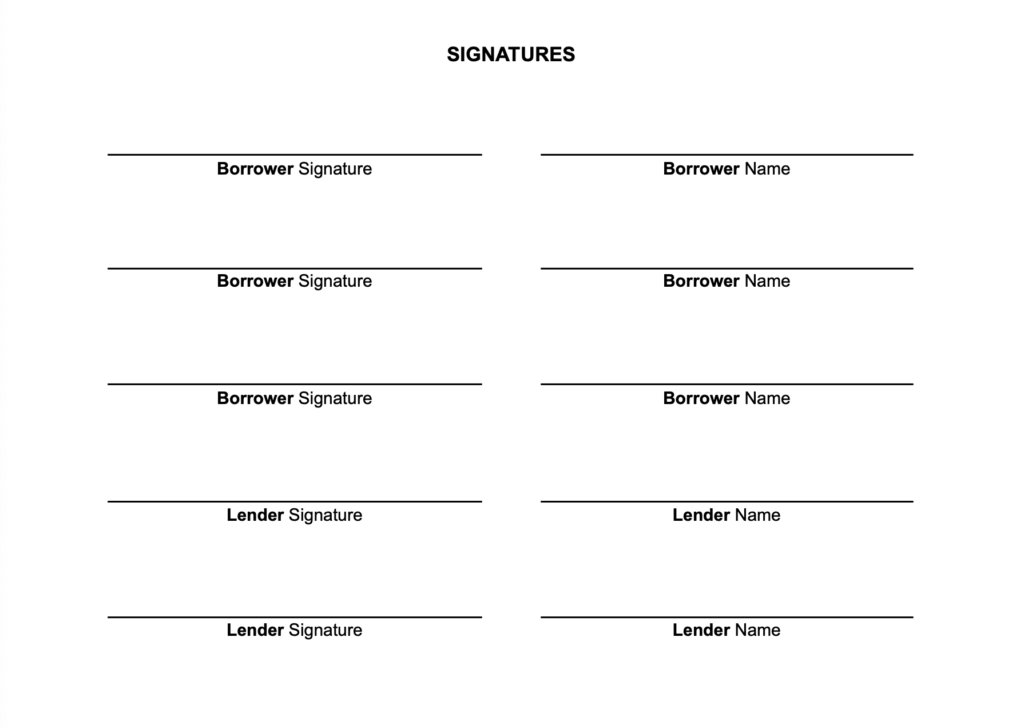

18. Signatures. Specify whether a notary public, witnesses, or both will acknowledge the agreement.

Before you sign your name, review your document thoroughly to ensure all the details are accurate.

Find a suitable individual to witness all parties sign the document. While some jurisdictions have different requirements for witnesses, a good candidate is generally someone who:

Ensure to acquire all relevant signatures. If there are multiple borrowers or lenders, every party must sign for themselves.

Download a mortgage deed template as a PDF or Word file below: